There are several companies claiming to offer AI solutions to banks and financial institutions. We found that these solutions are intended to help banking and finance companies with at least one of the following business problems:

- Fraud Detection

- Product Development

- Operations

Diebold Nixdorf, perhaps best known for their ATM technologies, offers software for ATM maintenance, purportedly allowing banks to be notified when an ATM is due for maintenance before it malfunctions. C3.AI offers a similar software. Arimo offers fraud detection software, a common application of machine learning in finance. TrueMotion claims its IoT software can allow auto insurers to collect data on its customers with their permission to offer them more tailored insurance products based on their driving behavior. We discuss this application further in our broad report on AI in insurance.

That all said, the companies listed in this report all seem to lack available case studies showing success with their software, and some even fail to list clients for their software on their website. This either indicates nondisclosure agreements between the companies and their clients or, likely, that AI-based IoT solutions for the finance and banking sectors are relatively nascent. Finance and banking executives looking to start integrating IoT devices into their workflows and leverage AI along with them ought to read our executive guide detailing three rules of thumb for cutting through the AI hype and vetting companies on their claims to leveraging artificial intelligence.

Fraud Detection

Arimo

Arimo offers a software called Behavioral AI for Financial Services, which it claims can help financial institutions detect fraudulent or unusual customer behavior using anomaly detection.

Arimo describes their solutions as “Behavioral AI for IoT,” which would imply their machine learning algorithms can be applied to IoT devices to gather and analyze data for the industries they claim to serve. In addition to financial services, Arimo has solutions for the retail and industrial manufacturing spaces. Each solution must have its own algorithm made to analyze data from the IoT devices specific to the industry it is for.

For example, Arimo claims that its retail solution makes predictions based partly on data from customer eCommerce activity, which can see a record of each time a customer clicked on a product link or other site element. Their industrial and manufacturing solution allows for the automation of the tuning process on machinery products, and Arimo claims one of their clients is doing this with refrigerators. This would require the machine learning model to be trained on data from robotic assembly systems.

It is likely that Arimo’s machine learning model for its Behavioral AI needs to be trained on millions of bank transactions that are directly linked to the internet of things. This would include transactions made using a smart ATM, mobile app, a smart card, or a paywear item such as a KRing. Some of the transactions used for this training would have been labeled as either fraudulent or suspicious.

Transactions could be labeled this way if they contained incorrect information or if the information did not match what the client company’s system accepts to validate a transaction. A transaction could also be labeled as fraudulent if the customer used an ATM that they normally do not visit or if suspicious behavior was caught on the ATM camera. The machine learning model would then be exposed to the labeled transaction data. This would have trained the algorithm behind it to determine which transactions could be fraudulent.

A client company could then deploy Arimo’s Behavioral AI for Financial Services, and the software would then be able to identify fraudulent transactions just as they enter the client’s system. Subsequent transactions would keep training the algorithm behind the software as users accept or reject the software’s evaluations. This way, the software is able to “learn” new fraud methods as it helps the client.

It’s likely that a data scientist can integrate the software into the client company’s database where they store data from transactions using the Internet of Things. These transactions could be made from a mobile app or a smart ATM.

Our research yielded no results when we searched for a demonstration video showing how Arimo’s Behavioral AI for Financial Services works. Arimo does not make available any case studies reporting success with their software., but it lists Nasdaq as one of its past clients.

Christopher Nguyen is CEO at Arimo. He holds a PhD in Philosophy of Electrical Engineering from Stanford University. Previously, Nguyen served as CEO at Bluepulse.

Product Development

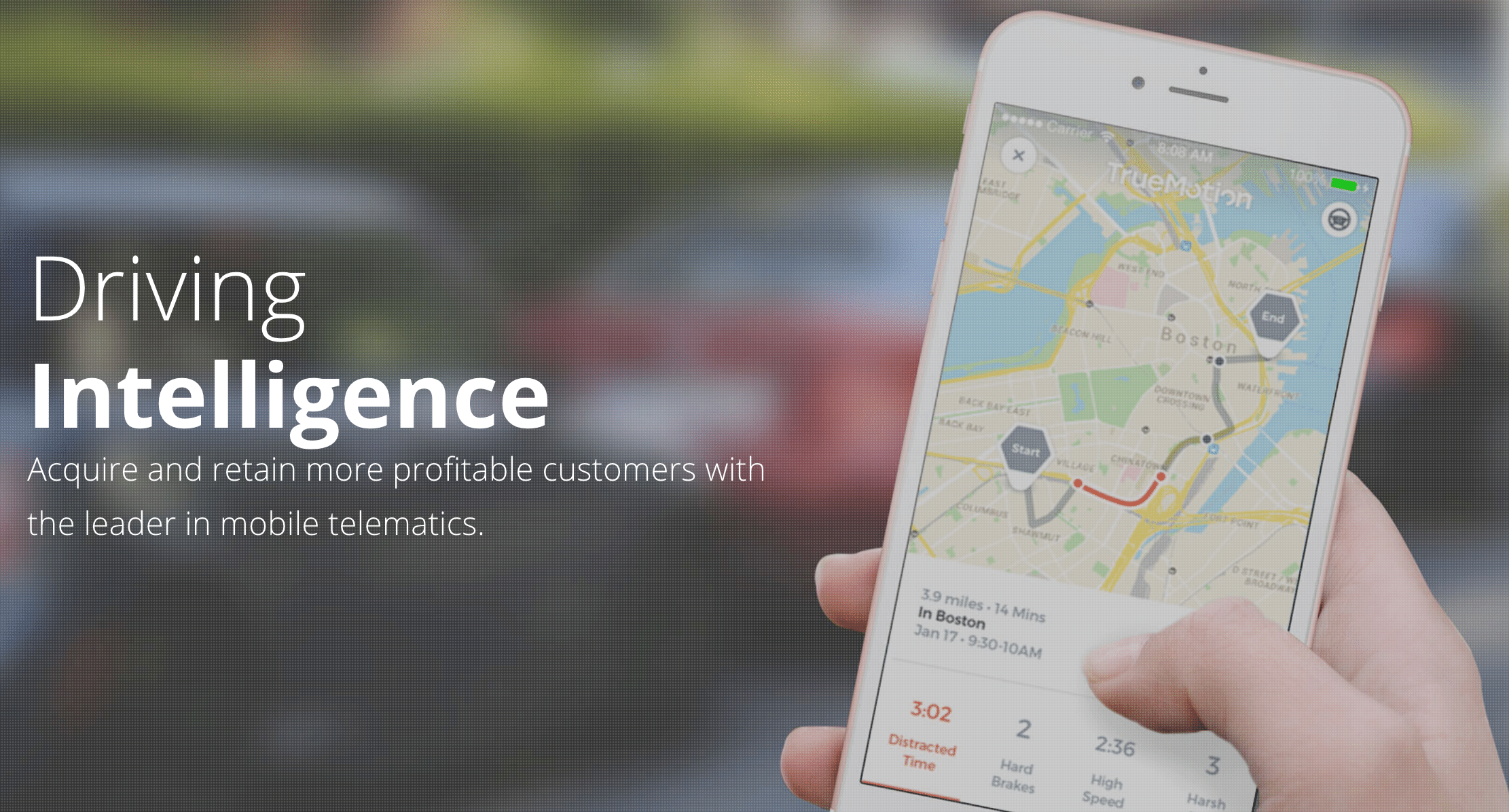

TrueMotion

TrueMotion offers behavior change algorithms, which it claims can help auto insurance companies offer more tailored products to customers based on their behavior using predictive analytics.

Insurance companies can have their clients use the TrueMotion mobile app or a TrueMotion-integrated company app to detect changes in driving behavior. The algorithm utilizes sensors present in most smartphones to check when the driver is touching or using their phone, how many hard brakes they make per day, and their daily mileage. This activity is then used as data to determine how much risk the driver poses to the insurer, based on the frequency of the activity and how long the driver is spending on their phone each time they touch it.

Progressive Insurance used TrueMotion’s solution for their Snapshot Mobile app when transitioning from their previous ODB device that plugged directly into the driver’s car. The mobile app serves as a replacement for the ODB device, though users can still choose to use older device to obtain discounts from Snapshot. Both the mobile app and ODB device process driving data, and in turn help progressive gather information about their clientele’s driving behavior. For at least Progressive’s instance of the TrueMotion solution, this is likely to help the behavior change algorithm assess risky driving.

We can infer the machine learning model behind the software was trained on tens of thousands of data points from car trips where the software was in use. The data would then be run through the software’s machine learning algorithm. This would have trained the algorithm to discern which data points correlate to distracted driving, risky or reckless driving, or other behavior that would indicate a higher risk posed by the driver.

The software would then be able to predict if a customer’s insurance payment should be raised or lowered. This may or may not require the user to upload information about their flat rates and adjustment intervals into the software beforehand. For example, if a driver had an irregular policy that was part of an older promotion, that driver may be entitled to a lower adjustment rate for accidents and risky driving behavior.

We could not find a demonstration video available for the behavior change algorithm. TrueMotion does not make any case studies available that report success with their behavior change algorithm, but it does list Intact Financial Corporation and Nationwide as some of its past clients.

Brad Cordova is a Board Member and former CTO at TrueMotion. He holds an MS in Electrical Engineering and computer science from MIT. Previously, Cordova served as a Research Fellow at the California Institute of Technology.

Operations

Diebold Nixdorf

Diebold Nixdorf offers ATM as a Service, a multi-channel solution for banks which includes physical ATMs, asset financing services, fleet management for the ATMs, and a suite of supportive software partly backed by AI. Diebold Nixdorf claims their solution can help banks and financial organizations improve the productivity and security of their self-service ATM fleet using their smart ATMs and machine learning.

ATM as a Service is one of Diebold Nixdorf’s AllConnect services, which is their selection financial business services that allows organizations to implement, manage, and perform maintenance on their fleet of ATMs. A service to manage and make changes to individual business branches and their operations is also part of the AllConnect Services. However, ATM as a Service is the AllConnect solution that provides the physical ATMs and Diebold Nixdorf’s Vynamic software.

The software suite contains seven programs for use across the entire solution, but the most important is Vynamic Analytics. This single software leverages AI to extract business insights for recommendations on how to change operations to improve productivity and security at the customer level.

We can infer the machine learning model behind the software needs to be trained on millions of ATM transactions from the client company’s customer base. This data includes how many cards the ATM(s) declined, how long the transaction takes to complete, and the rate at which the ATM(s) are serving consecutive customers. The data would also include the customers’ ages segmented by generation. The data would then be run through the software’s machine learning algorithm. This would have trained the algorithm to discern which data points correlate to the most time spent finishing a transaction, the issues that resulted in the longest customer wait times or “congestion,” and the reasons for declining a card.

The software would then be able to measure how long each generation of customers is spending at the ATM screen, how much traffic the ATM is handling and at what rate, and the number of cards declined. Each of these measurements is called “Screen Dwell Time,” “Congestion Score,” and “Card Captures” respectively. The system may then be able to use these measurements to recommend changes to business operations in order to lower all of these values. For example, if customers across all age groups seem to be encountering the same ATM error when using their card for a withdrawal, the system may recommend repair for the ATMs where customers have encountered the error. This may or may not require the user to upload information about their future plans for business operations into the software beforehand.

Below is a short video demonstrating how Vynamic Analytics (then Vynamic Insights) works. The demonstration begins at 1:23 and continues until 7:20.:

Unfortunately, even Diebold Nixdorf does not make any case studies available reporting success with its software.

Ashvin Mathew is CTO at Diebold Nixdorf. He holds an MS in Computer Engineering from the University of Pennsylvania. Previously, Mathew served as General Manager at Microsoft Cloud and Enterprise and helped build Microsoft Dynamics 365.

C3.ai

C3.ai offers software called C3 Sensor Health, which it claims can help banks and financial institutions spend less on deploying IoT sensors for their equipment using predictive maintenance.

We can infer the machine learning model behind the software needs to be trained on tens of thousands of telemetric data points from IoT sensors attached to industry-specific equipment. In finance, this would include ATMs, smartphones using mobile banking apps, or payware devices like the KRing from Kerv. The data would then be run through the software’s machine learning algorithm. This would have trained the algorithm to discern which data points correlate to a sensor that is going to malfunction soon or has stopped working completely. For example, if a sensor starts to take longer to respond than usual and this problem persists across multiple checks, that sensor could be flagged as “could malfunction soon.”

The software would then be able to measure how many sensors have stopped working, how many sensors are likely to stop working soon, and how likely they are to stop working. The system may then be able to use these measurements to recommend which sensors are in the greatest need of maintenance. For example, the software could detect 15 malfunctioning IoT sensors on ATMs and 10 sensors that are likely to malfunction soon. The system would be able to show the user where those sensors are in relation to each other.

When the software creates the prioritized list of sensors that require maintenance, it could list the sensors by a combination of how much maintenance is needed and how close together they are. That way, a business leader can decide to deploy maintenance to a specific area where their sensors are and fix all problem sensors with a single appointment. This may or may not require the user to upload information about their current maintenance plans into the software beforehand.

Below is a short 3-minute video demonstrating how C3 Sensor Health works. However, it is worth noting that this demonstration uses an instance of the software customized for the utility industry and that some aspects may vary for the banking and financial spaces.:

C3.ai does not make available any case studies showing success with C3 Sensor Health.C3.ai does not list any major companies as clients, however, they have raised $228.5 Million in venture capital and are backed by Breyer Capital and Sutter Hill Ventures

Ed Abbo is CTO at C3.ai. He holds an MS in Mechanical Engineering from MIT. Previously, Abbo served as SVP of Applications at Oracle.

Header Image Credit: PYMNT